Categories

Friday update real estate blogPublished January 3, 2026

First Friday Update January 2, 2026

Happy new year!

As we start the next trip around the sun we as a brokerage are making some much needed changes. This is our new website which is part of a total overhaul of our back and front end systems. My goal this year is to make SRG into the shop I always wanted but was too busy to build. We took the slower time to make the changes that we needed to make and are stoked to take on 2026 with not just a boat load of experience but with some cool new tools too.

Anyways! Looks like in December we hit 871 total sales across the MLS for a median sold price of $460,000. Our peak sold price in 2022 was just over 500k so the fact that we're not even 10% off on the median price is kind of remarkable. Days on market are steadily rising and for last month median days on market was 48. Keep in mind this is for the houses that sold, there are many houses sitting on the market for months and not selling.

December of 2024 had a virtually identical sales count with a median sold price of $485,000. So we did come down a bit over the last 12 months, finally.

Currently available existing single family homes in El Paso County that you can go and buy today number at 1,698. This time last year we had 1,391. The year before that we had 950. So 2024 to 2025 saw about a 40% increase in listings to start the year and 2026 is kicking off about 22% higher than 2025.

Year over year comparison.

2024 total sales were 11,503 units. The lowest median sold price was in January of 2024 at 450k and then by mid summer our median sold price jumped to a high of 499k.

2025 total sales is approximately 11,751 maybe a little bit more as the last few sales from this week get closed out in MLS with holiday delays. Our lowest median sold price was December at 460k while our highest median sold price came in June at 500k.

For context 2020 and 2021 came close to 19,000 sales both years.

The median sold price is impacted by higher end homes selling more aggressively than lower end homes. We have a much weaker market below 700k than we do above it. So the volume of higher end homes selling and the volume of lower end homes not selling as well is skewing the median price higher and has been for the last 3 years.

In the spring of 2022 interest rates began to climb and peaked by Fall of 2022. Realtors and lenders alike were screaming from the roof tops to buy now and refinance in a year or two when rates come down. Rates have been incredibly steady over the last 3 years with no significant relief in sight..png)

Mortgage rates have been locked in a range so tight that even all the kids talk about it now. 6-7.

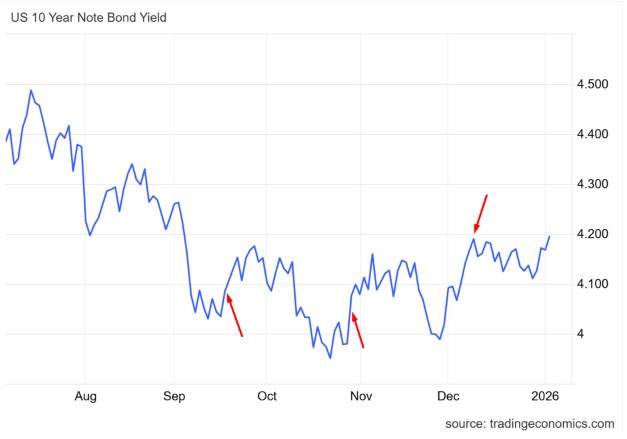

There has been plenty of hype regarding the Federal Reserve lowering interest rates. The Fed cut rates 3 times in 2025. That was in September, October and December. When the Fed cuts rates what we're talking about is the fed overnight funds rate. This is the rate that banks pay to borrow money for incredibly short periods of time and does not directly impact market rates on things like treasuries or mortgages. Just to prove this point look at the graph of the US 10 year treasury yield with the red arrows indicating the dates of the recent rate cuts.

So what we can say with a pretty high degree of certainty is that the rates are where they're at and have been for the last 3 years. The anticipation and pressure for further rate cuts is contradictory to the overall economic data. We just posted 3.8% GDP growth which truly is a remarkable number. So the issue is that if the economy truly is doing as good as the data suggest than there really is no basis for lowering rates any further. The Fed chair Powell and several others have indicated that the Fed at this point sees their interest rate policy as neither accommodating nor restrictive, aka neutral. The suggestion from the Fed at this point is that they don't want to cut rates too much as they worry that will trigger higher inflation numbers. However politically there is pressure from the top to lower rates to stimulate the housing sector which has for sure been lagging over the last 3 years.

Let's assume that interest rates remain relatively steady where they're at now. Let's assume that demand remains roughly where it is as well. Let's talk about supply.

As I pointed out earlier supply has been steadily increasing since the bottom of 2021. We have some serious structural shifts happening that will contribute to a further increase in supply this year.

First and foremost foreclosures. They're finally making a come back and this is a very good thing. In 2024 we had just over 600 foreclosures. In 2025 it looks like we will finish the year with around 900. Kicking off 2026 I'm seeing more foreclosures hitting the market than I have since probably 2014. Why is this a good thing? It's a good thing because sometimes it takes some short term pain to keep the market healthy and honest.

The policy of forbearances and foreclosure prevention that started off in 2020 and lasted until October of last year has protected a few unfortunate people while artificially supporting inflated real estate prices for the rest of us. This policy has created a back log of foreclosures that are just now starting to finally make their way to market. How many are out there we have no real way of knowing but one thing is true. If demand stays flat and supply increases we will see prices go lower. As prices go lower more and more distressed properties will find themselves upside down causing even further pressure on pricing. Allowing this to happen is important as markets need to find their own tops and bottoms to have true price discovery. Allowing markets to crash ultimately is what keeps them healthy and honest as value seeking buyers will always mark the bottoms with increased buying to begin the next rebound.

I do firmly believe that foreclosures in the next two to three years will make a noticeable impact on the housing market. This will be by further saturating supply with houses that absolutely have to and will sell.

A second source of increased inventory is that sellers simply can not wait forever for lower rates. I have personally seen this and can see it across the market. Sellers who didn't list in 2023 or 2024 because they were hoping to hold out for better interest rates often did list in 2025. Sometimes life moves on even when the conditions aren't perfect. And as the anticipation of lower rates fades people continue to live life and seek opportunity. This will continue in 2026 I believe.

A third and potentially least reliable source of more inventory would be the institutions. These are the hedge funds and iBuyers etc. While these companies were aggressive buyers leading up to and exploding through 2020 and 2021 they have been net sellers since. It will be interesting to see how much of their portfolios are for the long hold and how many they will liquidate this year. It's tough to get data online for exactly how many homes companies like this own but a quick search of "HPA" in the assessor records maxes out their 300 unit search maximum. I'll be going to the assessor's office Monday for some reconnaissance and see if I can get the real number there in person.

The fourth source of inventory of course are the builders. Builders right now are about as generous as I've ever seen it. Where as in 2021 or 2022 builders were charging lot premiums and mark ups across the board today we see incentives of upwards of $100,000 on houses. The builder hustle is to protect their price while giving away a ton of incentives. This way if the market strengthens up they remove their incentives and can argue that the price is the price. The builders set their own comps in the communities they build in and do whatever they can to steady their pricing even if it means huge incentives for rate buydowns, upgrades or even debt reduction for VA buyers.

What's interesting though is that you have examples in some of these communities of foreclosures already competing in the resale market. One specific example from the real is something my partner is working on right now. This particular house built in 2022 sold back then on a VA loan for 611k. This house 3 years later has been on the market for almost 3 months and is priced below 515k. And this same floor plan is still being built by this builder just down the street. So as a buyer walking into the builders office and knowing that a foreclosure that's just 3 years old is sitting at 100k less than it sold for new 3 years ago might buy you some leverage with that builder. The way that increasing foreclosure volume specifically in new build communities will impact builders is something I'm curious to see. For me in my 12 plus years this is my first time witnessing this dynamic and genuinely I'm curious to watch it play out.

To sum it up, what housing shortage? We have 22% more homes for sale than a year ago. Over double what we had 2 years ago. And over 8x as many as we did at the start of 2021. What we need to see is the market find its bottom over the course of the next however long it takes. We're certainly seeing signs especially towards the lower end of pricing that sellers are willing to capitulate. We had a deal a couple weeks ago close where we had the buyer. House was listed at 400k. 3 years ago it would have sold for that in a weekend. Our agent locked that house up for the buyer at 355k with another 25k in closing costs paid out by seller. So net 70k less than it would have brought 3 years ago.

I closed one buyer side a couple months ago where we got the house for about 60k below the original asking price and with the purchase got a new roof, new sewer line, new electric panel and a fully remodeled home.

The deals are starting to come together more and more often and starting to really favor the buyers. If you've been thinking about making a move probably really start thinking about it. "The bottom" of the market is something that we figure out a year or two after it happens so there's no way to time it right. If you have a long term view on real estate and are willing and able to endure some volatility over the next few years this is becoming the friendliest market towards buyers that I've seen in at least 10 years. I'm not saying hurry up and buy, matter of fact I think this market will very much reward patience. I do think that opportunities for buyers will be more and more appealing as we move through 2026.

That being said if you've been on the fence about selling we're still coasting a solid 50% or so above pre covid pricing. Despite the slowness of it all houses are still selling and selling near record pricing when represented by the right agents. The truth is during 2009 in the pits on the housing break down things still sold and they always will. It's just about positioning yourself in a way to take advantage of the market rather than the opposite.

My goal for 2026 is to get back to my roots in real estate. This and only this. I learned a lot over the last 3 years splitting my time with construction and truth be told the best mistakes are the ones you learn from. I've learned what I needed to learn. I'm better off with the connections I've made. I'm stoked about what I'm able to do for my real estate clients and most of all I'm stoked to fully focus on the one thing I'm really good at.

That's taking care of your real estate needs.

Happy new year and let me know what we can work on together!

|

or another way